As the events of the last few years in the real estate industry show, people forget about the tremendous financial responsibility of purchasing a home at their peril. Here are a few tips for dealing with the dollar signs so that you can take down that “for sale” sign on your new home.

Get pre-approved. Sub-primes may be history, but you’ll probably still be shown homes you can’t actually afford. By getting pre-approved as a buyer, you can save yourself the grief of looking at houses you can't afford. You can also put yourself in a better position to make a serious offer when you do find the right house. Unlike pre-qualification, which is based on a cursory review of your finances, pre-approval from a lender is based on your actual income, debt and credit history. By doing a thorough analysis of your actual spending power, you’ll be less likely to get in over your head.

Choose your mortgage carefully. Today, the average person will accumulate debt due to credit cards, student loans, etc.

We believe the right time to purchase a Home is when you are debt free and ideally have a down payment of 20% to avoid paying PMI (mortgage insurance).

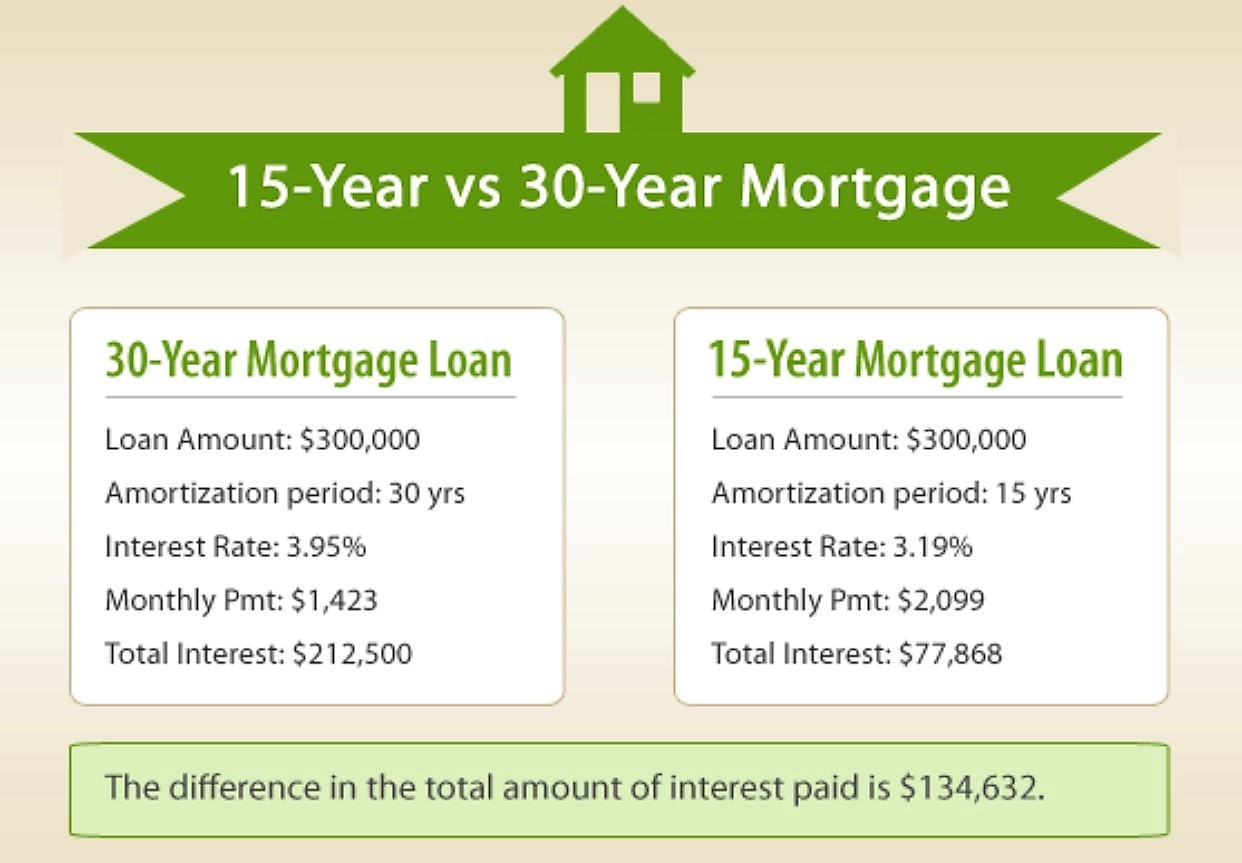

Instead of buying your dream home, purchase a modest Home you can afford with total monthly outgoings no more than 25% of your income. If you finance it on a 15 year fixed interest rate mortgage instead of a 30 year mortgage you will also save yourself a ton of money in interest. The shorter the term, the better interest rate you will be offered.

For Example:

At Fahy Real Estate we are huge advocates of the Dave Ramsey system and believe strongly in his philosophy.

Do your homework before bidding. Before you make an offer on a home, do some research on the sales trends of similar homes in the neighborhood with sites like Zillow. Consider especially sales of similar homes in the last three months. For instance, if homes have recently sold for 5 percent less than the asking price, your opening bid should probably be about 8 to 10 percent lower than what the seller is asking.